Click image to enlarge

This was the COVID quarter, and the nation suffered the worst kind of loss. By the end of the quarter, the number of lives lost to the COVID-19 virus in the United States topped 125,000. The balance of this presentation is about the financial impact of the COVID crisis, but acknowledging the loss of so many Americans is the right place to start. The suffering and loss of our fellow Americans is as incomprehensible as it is incalculable.

Click image to enlarge

The second quarter opened amid rampant fear on Wall Street. Only six weeks before the quarter began, on February 19, 2020, the Standard & Poor's 500 had broken its all-time high price, and the longest bull market and economic expansion in modern history seemed like it might just keep on going. Then came the swift COVID bear market. From its February 19 record high to the bottom of the COVID bear market on March 23, a week before the second quarter began, the S&P 500 plunged 33.9%. Of course, no one knew that would be the bottom, and the second quarter was marked by sharp volatility.

Click image to enlarge

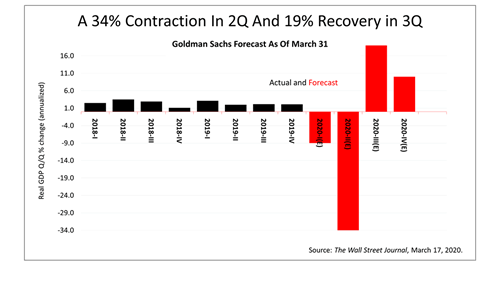

When the first quarter ended on March 31, 2020, Goldman Sachs was forecasting a second-quarter contraction of 34% in U.S. gross domestic product, far worse than any recession in modern U.S. history.

Click image to enlarge

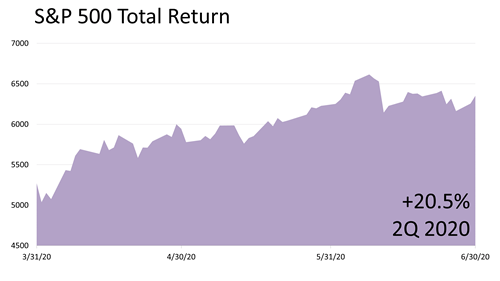

Here's how the quarter ended: Stocks posted a +20.5% gain in the second quarter of 2020, following a -19.6% loss in the first quarter of 2020. Not to belabor the point, but the takeaway is important: The second quarter started amid rampant fear and the stock market recovered in stunning fashion. That unpredictable twist of fate is why the investment discipline imposed by modern portfolio theory (MPT) is so important.

Click image to enlarge

Modern portfolio theory is a large body of financial knowledge based on academic research done over the last 70 years. This framework for investing is now taught in the world's best business schools and embraced by institutional investors.

Click image to enlarge

In addition to classifying investments based on their distinct statistical characteristics, MPT imposes a quantitative discipline for managing money based on history and fundamental facts about finance. MPT is an important framework for managing that risk, the risk of what might happen, but it does have its limitations.

Click image to enlarge

MPT is always looking backward, and not enough statistical history exists to predict markets reliably. To navigate the road ahead, you can't only rely on your rearview mirror!​ A professional practitioner combines the statistical framework of MPT with judgment and an understanding of current conditions to come up with a forward-looking view of the world. With that very big caveat, here's what happened last quarter.

Click image to enlarge

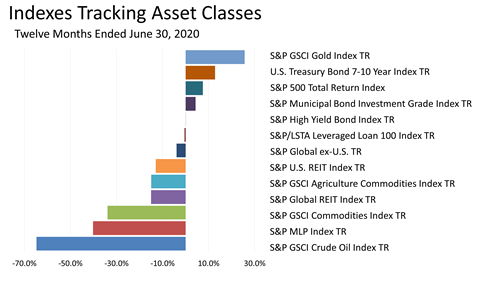

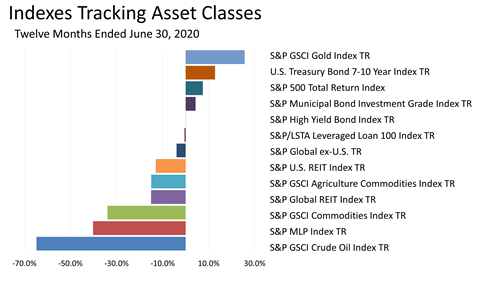

This is a snapshot of the anomalous performance of market indexes in the three-month recovery period after the COVID crisis bear market hit. Every quarter, in providing the three-month market index data, this quarterly market summary often reminds you that three months don't tell you much. Last quarter illustrates why three months of performance data are unimportant. The 20.5% return on the U.S. large-cap stocks in the S&P 500 in the second quarter is spectacular, but it does not incorporate the 33.9% plunge from the all-time high in stock prices on February 19, 2020. It's wise to view this three-month surge in the context of a bear market recovery. As you would expect in an economic recovery, growth stocks sharply outperformed value stocks. The U.S. stock market outperformed the other major global regional markets. Twelve of the 13 asset classes represented by securities indexes showed a gain in the second-quarter recovery. With checks of $1200 and an extra $600 in weekly unemployment benefits, the CARES Act boosted the economy starting in early April. With those government transfer payments – translate that as long-term U.S. debt – consumer discretionary stocks gained 32.9% and technology company shares returned 30.5%.

Click image to enlarge

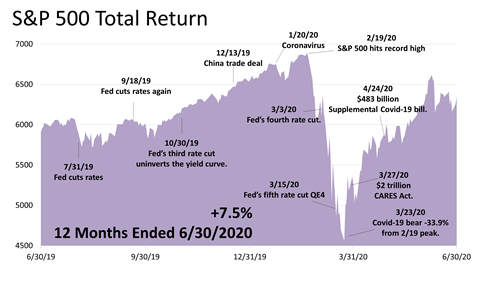

Over the 12 months ended June 30, 2020, the S&P 500 total return was 7.5%, but it was a wild ride. Stocks had risen steadily from July 2019 to an all-time high on February 19, 2020, when the brutal one-month COVID 19 market collapse occurred, bottoming after a -33.9% plunge.

Click image to enlarge

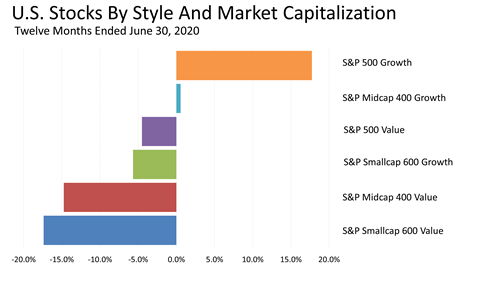

The chart reveals an uneven recovery in stocks that occurred in 13 weeks after the COVID-19 bear market bottom on March 23, the 12-month period through June 30, 2020. The S&P 500 composite was up 7.5% in the 12-month period shown. But the S&P 500 comprises the six sub-indexes shown here, and the large-company growth stocks dominated the composite's performance. To be clear, the positive returns in the S&P 500 were concentrated almost entirely in the S&P 500 index representing growth stocks. The 17.7% total return in the S&P 500 Growth stock index propelled the recovery, but four of the six sub-indexes of the S&P 500 composite sustained losses in the 12 months through the end of June. The S&P 500 composite index does not equally weight the performance of all 500 companies. It's a capitalization-weighted index, which means the performance of the largest companies influences the index more than the smaller companies.

Click image to enlarge

Apple, Microsoft, Amazon, Google, and Facebook have the most influence on the broad S&P 500 composite, and those are the very companies that were growing fastest through the recovery from the pandemic, which magnified their influence on the S&P 500.

Click image to enlarge

The outsized influence of the giant tech stocks is especially evident in this 12-month period that includes the bear market and the 13 weeks of recovery, and some pundits have warned that the large tech stocks dominating the S&P 500's recovery are in a bubble, but the price-to-earnings ratios on these stocks are reasonable. Apple, for example, recently was priced at 2.2 times its PEG ratio. A PEG – or price/earnings to growth ratio is a stock's P/E ratio divided by the annualized growth rate of its earnings. The PEG ratio is used to determine a stock's value while also factoring in its expected earnings growth rate. It offers a more complete picture than the more standard P/E ratio and is a widely used stock valuation measure. The PEG ratios of the giant tech stocks dominating performance of the S&P 500 are well within their historical levels, which is key to understanding the anomalous performance seen in this chart.

Click image to enlarge

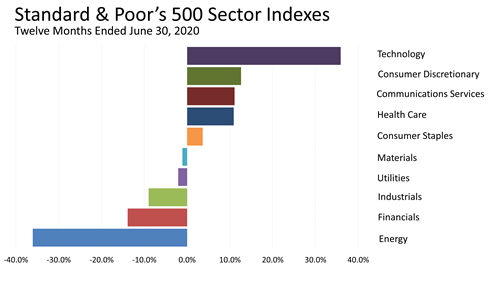

With a total return of 35.9%, the domination of the tech stocks in the 12 months ended June 30, 2020 is also clear from this chart. Of the 10 Standard & Poor's industry sectors, consumer stocks, along with heath care, also showed good returns. The big losers were energy stocks, which suffered a setback due to an oil price war between Saudi Arabia and Russia, and then were pounded again by the stay-at-home orders after the COVID outbreak.

Click image to enlarge

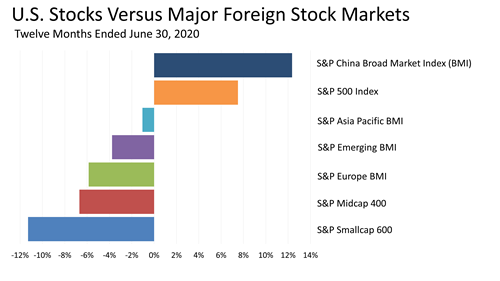

The S&P China Broad Market Index outperformed the world's major regional equity markets in the 12-month period ended June 30, 2020. China's fledgling stock market is subject to liquidity injections by the Chinese government. This one-year period encompasses the COVID outbreak, which hit China months before the virus struck the U.S. Chinese stock prices declined when the virus hit China, but by only about half as much as in the U.S. Keep in mind that over the long U.S. economic expansion from April 2009 through March 2020, the Standard & Poor's 500 outperformed Chinese stocks as well as the major equity markets across the rest of the world and emerging markets.

Click image to enlarge

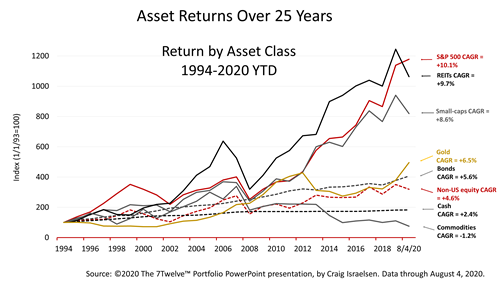

For the 12-month period ended June 30, 2020, the Standard & Poor's Gold Index was No. 1 among this broad array of indexes representing 13 different asset classes. Gold in the 12 months returned 25.7%, sharply outperforming the S&P 500 stock index's 7.5% return in the same period.

Click image to enlarge

Gold has not been a good investment over 25 years, compared to U.S. stocks. Compared to the 10.1% compound annual growth rate of the S&P 500 stock index over the last quarter century, gold returned just 6.5%. A major reason for gold's sub-par performance is that inflation has been running at less than the Federal Reserve Board's target rate of 2% for a decade. In the past, gold appreciated in inflationary periods, but inflation came down after the COVID crisis to one-half of 1% and is not expected to perk up in the foreseeable future. Despite its lackluster performance over the long haul, gold has been touted perpetually, probably since before the first coins were created thousands of years ago. Like the proverbial broken clock that gives the correct time twice a day, the gold bugs were right last year. Note: ©2020 The 7Twelve ™ Portfolio PowerPoint presentation, by Craig Israelsen. Used with permission. Indexes used in this illustration: Large-cap US equity represented by the S&P 500 Index. Small-cap US equity represented by the Russell 2000 Index. Non-US equity represented by the MSCI EAFE Index. Real estate represented by the Dow Jones US Select REIT Index. Commodities represented by the Goldman Sachs Commodities Index (GSCI). As of February 6, 2007, the GSCI became the S&P GSCI Commodity Index. U.S. Aggregate Bonds represented by the Barclays Capital Aggregate Bond index. Cash represented by 3-month Treasury Bills.

Click image to enlarge

It is perilous to predict the future of gold prices, the stock market, or other asset prices reliably, but gold could continue to perform strongly in the months ahead. Despite years of underperformance and no signs of inflation on the horizon, current financial economic conditions could be favorable for gold.

Click image to enlarge

Gold is a comparatively small asset class. The above-ground stock of gold worldwide, excluding jewelry, at the recent price of about $2,000 an ounce, is worth about $6 trillion according to the Federal Reserve Board's latest Financial Stability Report, released in May 2020. That's a fraction of the total value of the U.S. stock market of $38 trillion, and that's just U.S. stocks. It does not include equity markets outside the U.S. Meanwhile, the two most fundamental investments – stocks and bonds – are not screaming buys. With interest rates low and the Fed stating publicly that it does not expect to raise interest rates anytime soon, the low yields on bonds are not very compelling and stocks are trading at the high range of their historical valuation range. This could push money into gold, and it would not take much of a shift of capital from the huge stocks or bonds to drive up prices in the relatively small gold market.

Click image to enlarge

Other takeaways from the 12-month performance of the 13 asset classes represented here through June 30, 2020: The 12.8% total return on intermediate bonds. The Fed cut rates five times in the 12-month period, which boosted seven- to-10-year U.S. Treasury bonds' prices. With low inflation and a recovery of the economy paramount to the Fed, the one-year results on U.S. intermediate Treasury bonds are a good time to remind you that past performance is not indicative of future results.

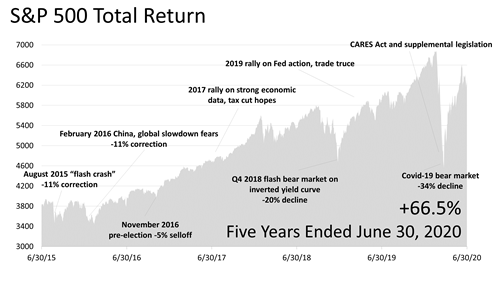

After trading sideways for about two years in 2015 and most of 2016, hitting two air pockets during that period, the stock market broke out of that range after the November 2016 election and rose steadily to a new record on September 20, 2018, whereupon it nosedived -20% on fears of an inverted yield curve. On January 4, 2019, the Fed signaled rates were on hold. That made stocks more attractive and prices rallied for most of the remainder of 2019. On February 19, 2020, the S&P 500 hit a new record, right before the COVID-19 virus put the economy and the stock market into a meltdown. By the end of the second quarter of 2020, most of the losses from that meltdown were recovered following enactment of the CARES Act and related legislation that have propped up the economy. Over the last five years, including dividends, the S&P 500 total return index has gained +67%. The five-year gain of +67%, or +13.4% per year, is more than the stock market's long-term annual total returns of approximately +10% going back 200 years, as described by Wharton professor Jeremy Siegel in his seminal book, Stocks for the Long Run, first published in 1994.

Click image to enlarge

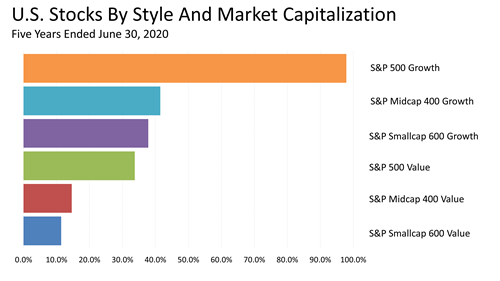

In the five years ended June 30, 2020, large-cap growth almost doubled, showing a 97.9% return. This compared to the 11.4% return on small-cap value. The disparity is caused by the domination of the “FAANGM†– Facebook, Apple, Amazon, Netflix, Google and Microsoft. With AMZN up 500%, MSFT up 350%, AAPL and NFLX up 300%, it's no wonder that large-cap growth was up 100% in this this five-year period. The stunning outperformance of these stocks in recent years and recent acceleration they've experienced during the pandemic, in combination with the fact that the S&P 500 Growth index is capitalization-weighted, has created this huge disparity between returns of large-growth and small-growth companies.

Click image to enlarge

Here again, you can see how the Tech sector, too, has contributed to large-cap growth's surge. By contrast, Energy, Financials, Materials, and Industrials – on the value side of the ledger – have lagged badly.

Click image to enlarge

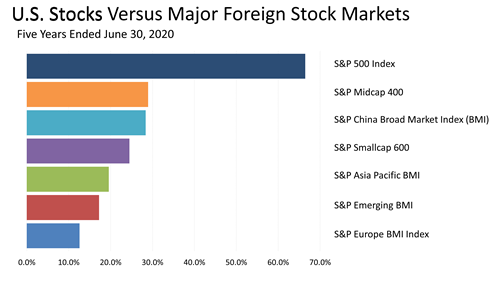

The S&P 500 has beaten major regional and emerging markets from across the globe consistently since the recovery from the global financial crisis in early 2009, and the U.S. stock market is leading world equity markets in the recovery from the pandemic, which is reflected in this five-year snapshot.

Click image to enlarge

For the five-year period ended June 30, 2020, the total return of the S&P 500 was 66.5% and was No. 1 among this broad array of 12 other asset classes represented by these indexes. Gold was No. 2. It was the third quarter in a row in which Gold was No. 2 in the list of asset classes by return for the previous five years. The S&P GSCI Crude Oil Total Return index lost nearly 80% of its value in the five-year period. Master limited partnerships, which own energy assets, lost about half their value in the period.

Click image to enlarge

|